The problem statement

The industry has spent a decade trying to optimize checkout, and the results have plateaued.

Despite continuous improvements in UX, speed, and interface design, cart abandonment has remained structurally high. The Baymard Institute continues to report average abandonment rates hovering around 70% globally, a figure that has shown little meaningful decline over time.

If incremental optimization worked, this number should have moved. But it hasn’t, because checkout failure is no longer driven by visible friction alone. It is driven by misalignment between user intent and system behavior at the moment of transaction.

Checkout funnel optimization is the discipline of removing every layer of technical, psychological, and design friction between cart initiation and order confirmation. In 2026, that means tight architectural alignment between your frontend, your commerce platform, and your real-time data layer. Done right, Baymard’s own benchmarking shows the average large-scale eCommerce site can lift conversion rates by 35.26% through checkout redesign alone, translating to $260 billion in recoverable revenue across US and EU markets.

What changes everything in 2026 is not the interface. It is the intelligence layer behind it.

The Behavioral Signal Problem Nobody Is Solving

Most eCommerce teams are still optimizing for the average user. They build a checkout that works reasonably well for a hypothetical buyer: logged in, on desktop, no pricing anxiety, familiar with the brand. That buyer is a minority of their actual traffic.

The real traffic looks like this: a mobile-first shopper three sessions deep who has compared the product twice, a first-time visitor from a paid ad who has not established any trust, a repeat customer whose last purchase was 14 months ago. Each of them needs a different checkout experience. A static page cannot serve all three. A behavioral signal-driven checkout can.

This is the structural shift happening in 2026. The checkout is becoming an output of real-time data, not a fixed template. And the brands engineering it that way are converting at rates that make the 70% abandonment benchmark feel like someone else’s problem.

What "Behavioral Signal-Led" Actually Means at Checkout

Behavioral signals are the real-time and historical data points that reveal intent, anxiety, and readiness to purchase. At the checkout stage, the relevant signals include device type and session behavior, payment method history, number of prior sessions before this cart, geographic location and payment preferences, scroll depth and hesitation time on specific fields, and whether the session originated from a retargeting touchpoint or organic search.

A checkout that reads these signals does not show the same experience to every shopper. It adapts. A returning Apple Pay user on mobile does not see manual card entry fields as the primary option. A first-time visitor from Germany does not encounter a dollar-only price without a currency switcher. A shopper who has hesitated twice on the payment step gets a trust layer injected, not a coupon code popup.

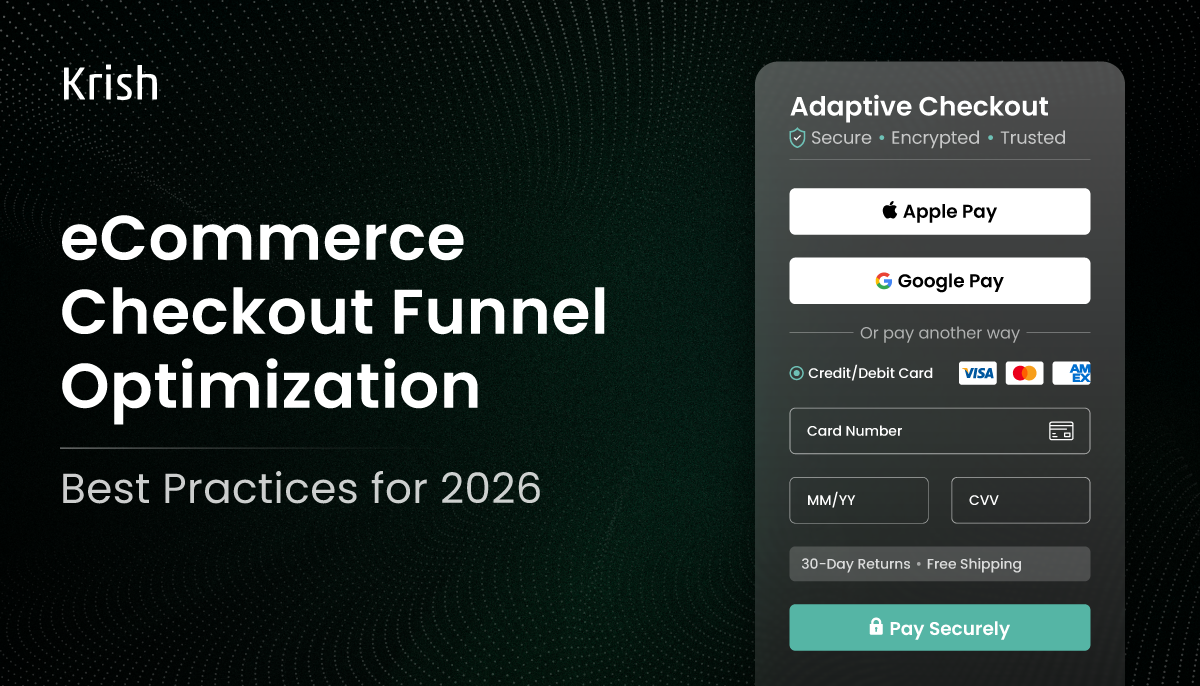

According to Worldpay’s 2026 Global Payments Report, digital wallets now handle 53% of all global eCommerce transactions, overtaking credit cards (16%) and debit cards (10%) combined. There are now 5.2 billion digital wallet users globally. A checkout that still presents manual card entry as the dominant payment path is not optimized. It is misaligned with how the majority of the world actually buys.

The behavioral signal layer connects what you know about the shopper to what the checkout shows them. That connection is the optimization. Everything else is cosmetic.

The 5 Dimensions of a 2026-Ready Checkout

1. Payment Method Intelligence: Show What the Buyer Already Uses

Static payment grids are over. The highest-converting checkouts in 2026 dynamically reorder payment options based on behavioral and geographic signals. A shopper on an iPhone with Apple Pay stored sees wallet authentication first, card fields second. A buyer in the Netherlands sees iDEAL as the lead option. A cross-border transaction from Southeast Asia surfaces the right regional wallet, not a generic card form.

This is not personalization in the marketing sense. It is payment stack intelligence applied at the moment of highest intent. And it removes the friction that 13% of abandoners cite as the specific reason they leave: their preferred payment method was not available or visible.

J.P. Morgan Payments’ 2026 Commerce Solutions report from NRF illustrates where this is heading: Sephora deployed J.P. Morgan Payments’ full-stack omnichannel SDK across US stores, enabling associates to accept payments anywhere in-store via Tap to Pay on iPhone, connected to the same identity and loyalty profile operating at the online checkout. The payment intelligence layer does not reset between channels. It follows the customer.

2. Trust Architecture: Place It Where Anxiety Peaks, Not Where It Looks Good

Trust signals placed in headers or footers are design choices. Trust signals placed at the exact point of peak shopper anxiety are conversion architecture.

In a standard checkout flow, anxiety peaks at two points: when the shopper sees the final order total for the first time, and when they are about to enter payment credentials. These are the insertion points for trust. Security indicators adjacent to card input fields, return policy microcopy directly beneath the CTA, a persistent order summary that never disappears as the buyer scrolls. These are not decorative. They are designed to resolve the specific objection the shopper is forming at that moment.

Baymard’s checkout research finds that 19% of shoppers abandon specifically because they do not trust the site with their payment information. That is not a design problem. That is a trust signal placement problem. The fix is architectural, not aesthetic.

3. BNPL Placement: The Decision Happens on the Product Page, Not at Checkout

Buy Now, Pay Later (BNPL) integrations positioned inside the checkout step are solving for the wrong moment. By the time a shopper reaches payment, the mental accounting of the full price has already happened. The reframing from $400 to $100 today needs to occur earlier, on the product detail page, before the psychological cost of the full basket is established.

The growth signals that buyer behavior around installment-based purchasing is already mainstream. Treating BNPL as a checkout option rather than a product discovery tool means arriving too late to influence the decision.

Surface the installment calculation on the product page. Let the shopper compute their commitment before the cart exists. By checkout, BNPL should feel like a confirmation of a decision already made, not a new offer.

4. Cross-Border Architecture: Revenue Is Being Left in Currency Gaps

Approximately 45% of global B2C eCommerce sales are now cross-border. According to Capital One Shopping’s 2026 research, 77% of consumers use multiple payment methods for cross-border transactions, because currency friction and trust concerns are higher across borders. A checkout that does not adapt to this is actively declining international revenue.

The practical checklist for cross-border checkout architecture: dynamic currency conversion triggered by IP location so shoppers browse and pay in their native currency, landed cost calculators that compute VAT, duties, and shipping tariffs before the final step, and locally preferred payment methods surfaced as primary options per region.

Klarna in Scandinavia. iDEAL in the Netherlands. Alipay and WeChat Pay in China. Pix in Brazil. The payment stack has to reflect where the buyer is, not where the brand is headquartered.

Surprise fees at the end of an international checkout do not just lose the sale. They create a trust failure that survives the session. The customer leaves and does not return.

5. The Data Foundation: A Checkout Is Only as Smart as Its Data Layer

Behavioral signal-led checkout optimization is not a design sprint. It is a data infrastructure project. The checkout adapts to the shopper only when it has access to a unified customer profile, real-time behavioral inputs from the current session, and a CDP or data layer that can activate both simultaneously.

Research from the CDP Institute’s 2024 Member Survey, covered in Krish’s MarTech Stack Audit analysis, found that 57% of organizations have unified customer databases. The remaining 43% do not. That 43% cannot build a signal-led checkout, not because of their front end, but because their data layer cannot support it. Personalization engines at the checkout layer run on identity resolution and behavioral history. Without a clean data foundation, what looks like a dynamic checkout is still a template with better copy.

This is why the Krish MarTech approach starts with the data layer before touching the checkout interface. The interface is the output. The data is the input. Fixing the output without the input produces a better-looking abandoned cart.

The diagnostic sequence matters as much as the fixes. Teams that start with solutions before completing the diagnostic fix the wrong things, spend the testing budget on the wrong hypotheses, and end up with a checkout that performs marginally better for a narrow user segment.

Step 1: Segment your abandonment data before reading it.

Top-line abandonment rate is a useless metric for diagnosis. Segment by device, traffic source, new versus returning visitor, and geography. A 70% abandonment rate on desktop from organic traffic and a 70% abandonment rate on mobile from paid social are two completely different problems with two completely different fixes. Funnel drop-off analysis that aggregates across segments produces conclusions that are accurate on average and wrong for every specific cohort.

Step 2: Map the behavioral pattern, not just the exit point.

A shopper who abandons at the payment step after 30 seconds is a different problem from a shopper who abandons at the same step after 4 minutes. The first suggests a trust or payment method mismatch. The second suggests a technical friction event: a failed validation call, a freezing field, a keyboard that collapsed on mobile. Session recording tools surface the distinction that analytics dashboards obscure.

Step 3: Form a hypothesis with a specific, falsifiable claim.

“We believe that surfacing Apple Pay as the primary payment option for iOS users will increase mobile checkout completion by 12% because current mobile abandonment at the payment step is 22 points higher than desktop, and iOS users have no visible wallet option without scrolling.” That is testable. “Let’s simplify the checkout” is not.

Step 4: Test server-side, not client-side.

Client-side A/B tests on checkout components introduce flicker, timing inconsistencies, and measurement gaps that corrupt results. Server-side testing via VWO, Optimizely, or similar platforms validates findings before they are committed to the codebase. Krish’s CRO and A/B Testing services operate on this methodology: every test is a structured experiment, not a design preference deployed to see what happens.

Step 5: Measure the full picture, not just conversion rate.

A checkout “optimization” that increases conversion rate while decreasing average order value is not a win. Track conversion rate, AOV, authorization failure rate, and post-purchase return rate together. The checkout that converts fastest is not always the checkout that generates the most revenue.

Where the Checkout Goes From Here

J.P. Morgan Payments’ biometrics research projects global biometric payment users reaching 3 billion by 2026, with transaction value at $5.8 trillion. Forms are already starting to disappear. Authentication is shifting to palm, face, and behavioral pattern recognition. The shopper who completed a purchase last month does not need to re-enter their card, verify their address, or answer a security question. Their presence is the credential.

J.P. Morgan’s 2026 payment trend analysis goes further: the emerging standard combines verified identity data with behavioral pattern analysis, moving fraud detection from rules-based models to continuous behavioral monitoring that runs invisibly inside the checkout session. The EU’s 2026 digital ID wallet introduction signals that authentication infrastructure at the government level is aligning with commerce-layer identity requirements.

What this means for checkout architecture today: the brands building toward a zero-form, identity-verified, behaviorally adaptive checkout now are building the infrastructure that will be table stakes by 2028.

The brands still testing button colors will spend that period trying to catch up.

The Honest Limits

Behavioral signal-led checkout optimization requires a data layer that most eCommerce teams do not have yet. A checkout that adapts to real-time CDP signals is not a Shopify theme update. It is a platform architecture decision. The implementation timeline for a fully decoupled, signal-responsive checkout is weeks of committed engineering, not a sprint.

In complex B2B environments, consumer-style streamlined checkouts actively break the buying process. A procurement manager navigating net-60 payment terms, approval workflows, and multi-destination shipping does not need a one-click checkout. They need a process that reflects how B2B purchasing actually works. Applying D2C optimization frameworks to B2B buyers is one of the most consistent and expensive mistakes in eCommerce optimization.

Legacy API debt also blocks progress that front-end changes cannot hide. A loyalty tier validation that takes six seconds through a SOAP API will create a six-second hesitation in the payment step, regardless of how well the React component above it is designed. The backend audit is not optional.

Closing

Krish has spent over 20 years engineering high-converting, MACH-aligned digital commerce ecosystems. From CRO audits that surface where your funnel is genuinely breaking to full MarTech capability builds that connect your data layer to your checkout intelligence, the work is architectural before it is cosmetic. The checkout you have today is a product of decisions made before behavioral signal technology existed at this scale. The checkout your competitors are building right now is not.

Frequently Asked Questions

Table of Content

Subscribe with Us!

Never miss any post, stay tuned!

Minal Joshi is a content marketer at Krish with a flair for eCommerce and Digital Commerce aspects. She is a MarTech fanatic with a knack of writing with which, she helps brands to curate, create, & commence digital brand positioning. Sharing insights via articles, case studies, eBooks, Infographics, and other forms of content creation is what she lives for. Being an ardent traveler, when not writing, you'll find her sipping coffee into the mountains or petting a stray.

Recommended Reading:

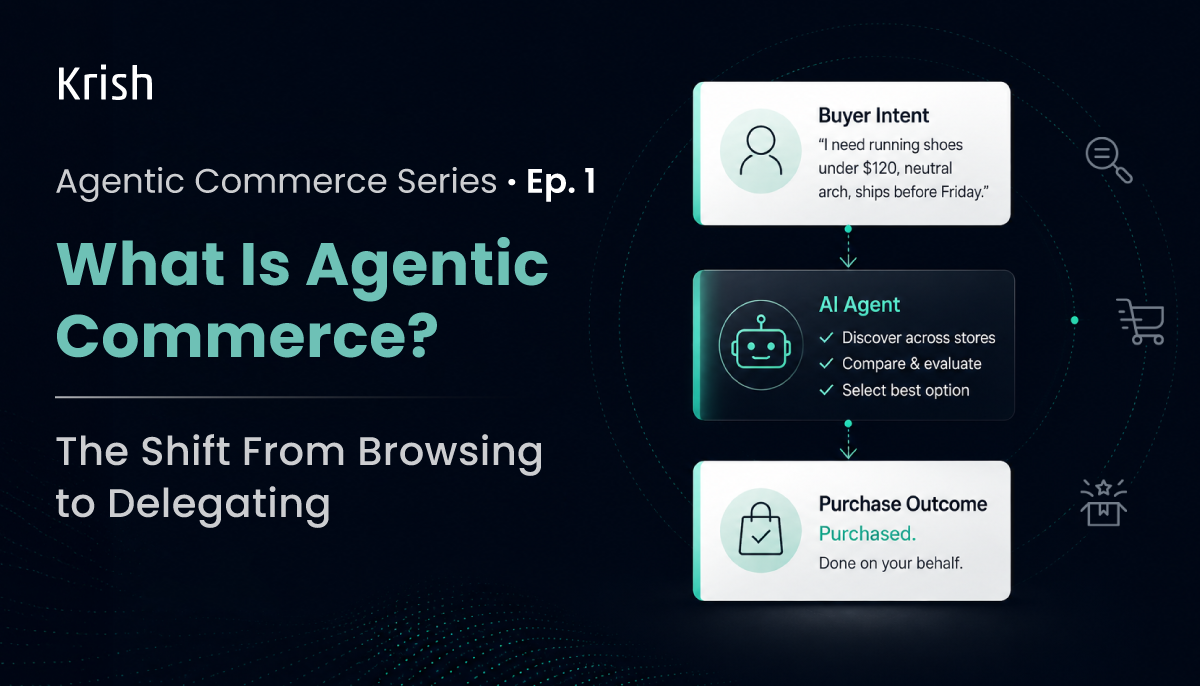

What Is Agentic Commerce? A Practical Guide for Ecommerce Leaders – Agentic Commerce Series | EP 1

22 June, 2026 That agent will research, compare, and buy on their behalf without clicking through your homepage, reading your PDPs, or experiencing your brand the way you designed it to be experienced. And when it is done, it will report back as “purchased”.

Subscribe with Us!

Never miss any post, stay tuned!

Trusted by leading brands